Reporting Methodology: Asking The Right Questions

“Like a pilgrim or a mendicant, I have moved on.

I have no right to inhabit your dreams,

to loom like a shadow on your patch of sunlight.”

- William Ayot

Businesses are awash in data. There are myriads of reporting forms, models, tools and management reporting techniques. Indeed, contemporary levels of automation have enabled reporting methodologies to evolve significantly. But the human aspect of reporting lags far behind. In many instances, data gives stakeholders essential signals to steer businesses in the right direction.

For example, management reporting shows 1) likelihood and magnitude of risk 2) financial performance 3) critical business indicators 4) timeliness in delivering expected results 5) correlation between variables and so on. Therefore, leaders can find any imaginable data ingredient to cook a delicious stew of management reporting. Leaders can easily track business performance pursuing deliberate strategies. However, there are many frightening instances of corporate and project failures. In fact, leaders are struggling to achieve expected results in terms of cost, time, benefits, quality and risk management.

Many practitioners and scholars try to explain these paradoxes by focusing on root causes. Nonetheless, they almost always investigate correlation without scrutinizing causality. Importantly, it is easy to fall victim to human heuristic, bias and prejudice when designing a management reporting approach. Relevant examples of bias include 1) rootedness in the status quo 2) action bias and 3) overconfidence bias. At the same time, technological, economic, aesthetic and political sublimes influence all aspects of management reporting, including a level of data transparency. Consequently, the report may purposely misrepresent the actual business situation.

There is ongoing debate about the best available management reporting set of lenses for business leaders. The essential principle to follow is this: no one paradigm is the best. Leaders should ensure that business control data reveals what stakeholders need to track and analyse, rather than reveal what is comforting to believe. The management reporting framework should help leaders grasp causality linkage and facilitate open dialog among key stakeholders, as well as visualize and track business performance. In a nutshell, reports should help leaders diagnose what they are up against.

In this respect, we advise leaders to ask three main questions:

1. What should be done with a particular reporting methodology?

2. What mechanisms and solutions do leaders already have in place?

3. What data has to be gathered and reported to stakeholders, in order to make unbiased and reasoned decisions?

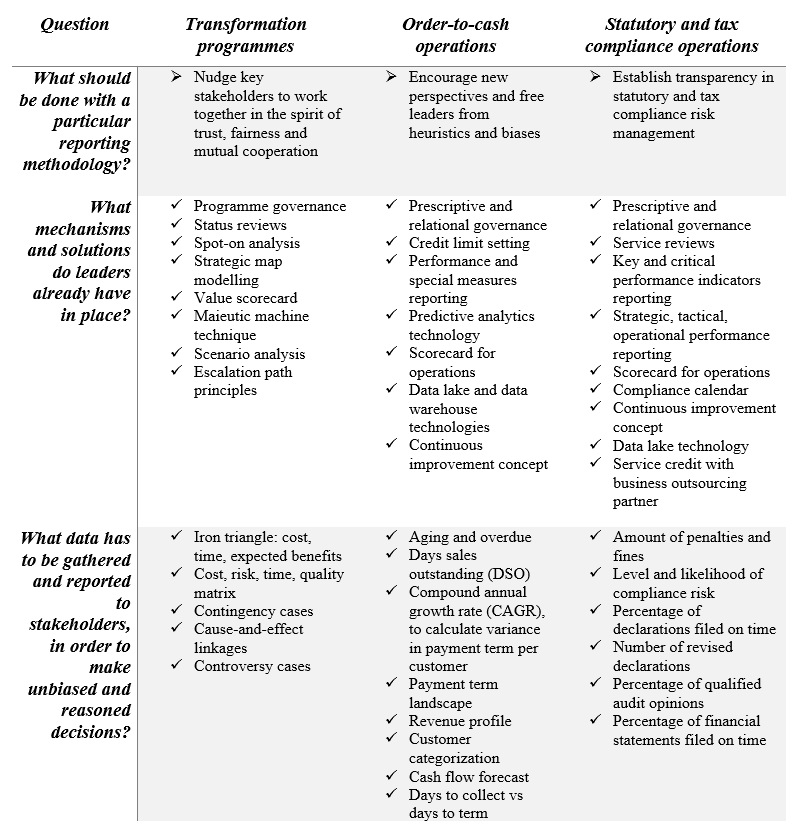

Table 1 shows empirical examples from 1) transformation programmes 2) order-to-cash operations and 3) statutory and tax compliance operations reporting methodologies.

Table 1 Empirical examples and three essential questions

As Macintosh and Quattrone (2010) explain, “Models and theories help us to see and understand things that we might otherwise overlook. However, by making some of this relationship visible and intelligible, they also obscure and exclude other possible vistas on management control problems. Therefore, we need to be acquainted with various forms of explaining and interpreting organizations and controls. Knowing one perspective only is too reductionist, given the complexity of the phenomenon” (p. 51).

Govindarajan (2016) adds, “If you proactively attend to the future every day, you earn the opportunity to shape the future to your advantage.” Leaders should use top-notch reporting methods, models and algorithms when assessing data. They should focus primarily on 1) constituents of the specific problem 2) performance of each business unit and 3) distribution of outcomes. Further, leaders should employ best practices in evaluating the performance of team members. However, properly designed management reporting is more than a simple representation of performable space. It is a method of ordering which encourages people to explore new solutions.

We agree that asking the right questions helps leaders to frame the reporting methodology as a tool. Also, it helps to structure dialogue with key stakeholders and design a proper reporting philosophy. And a proper reporting philosophy helps ensure that business will run successfully.

References

Govindarajan V. The Three Box Solution: A Strategy for Leading Innovation (Boston: HBR Press, 2016).

Macintosh, N. and Quattrone, P. (2010) Management Accounting and Control Systems: An Organizational and Sociological Approach, Hoboken, N.J.: Wiley.