Scorecard – A New Map to Steer Businesses

“The soul is here to find its own way -

to do what’s next, to experience.”

- William Ayot

It is seductive to assume that patterns in a numerical data set are accurate. Quattrone et al. (2016) observe that “management accounting and reporting tools need to constitute a method for ordering the complexities management faces and provide a means for scrutinising unknown unknowns in innovative ways when responding to corporate challenges”. How should leaders cope with the management reporting problem? In this article we propose two simple techniques for better management reporting – a balanced scorecard and a scorecard.

Let us begin by clarifying the terms. Kaplan and Norton (1992) define a balanced scorecard as a tool that “translates an organization’s mission and strategy into a set of performance measures that provides the framework for implementing its strategy”. Busco and Quattrone (2015) note that a balanced scorecard (BSC) is “…a framework for combining financial and nonfinancial performance measures and building explicit links between strategy, goals, performance measures, and BSC outcomes”. Quattrone et al. (2016) argue that a scorecard is “…any management accounting and reporting system that works as (1) a visual space for interaction; (2) a method of ordering and scrutiny; (3) a platform of mediation; and (4) a motivating ritual of engagement”.

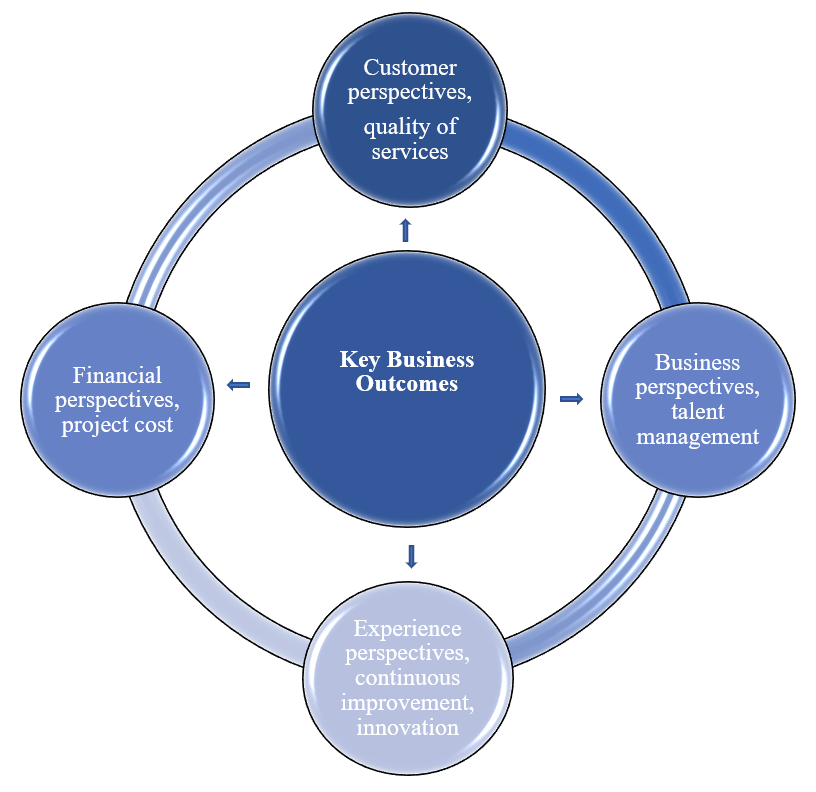

Ultimately, the reporting framework should explain how the business is governed, how contractors are performing and how priorities are defined. In Figure 1 we provide an example of a balanced scorecard leaders should consider when defining strategies. The figure provides a framework for improving decision-making and determining new directions. The priorities outlined in Figure 1 are by no means exhaustive.

Figure 1

The balanced scorecard (adapted from Kaplan and Norton, 1992)

The introduction of a balanced scorecard 1) improves management reporting 2) supports leaders coping with business uncertainties and 3) helps leaders address internal and external environment complexities. Even so, cause-and-effect linkages are merely hypotheses and are not precise -- a balanced scorecard rarely represents cause-and-effect linkages in business deliverables. Christensen et al. (2016) point out “the fallacy of conforming data: managers focus on generating data that conforms to their pre-existing business models”.

Based upon empirical experience, we propose ignoring the traditional balanced scorecard and in its place creating a scorecard. The scorecard equips leaders with eight cards: 1) strategic alignment with stakeholders 2) end-to-end process ownership 3) automation of operations 4) organisation design and sourcing model 5) service demand and quality 6) operating model and governance framework 7) internal control and risk management environment and 8) management reporting framework. The following figure provides an example of such a scorecard, which can serve as a strategic map to steer businesses.

Figure 2

The scorecard

Applying the scorecard improves management reporting systems. The scorecard not only encourages leaders to explore strategically important directions through dialogues with key stakeholders, but it also establishes a management reporting philosophy. Therefore, the scorecard helps define metrics to track business performance.

However, leaders should not attempt to create the perfect scorecard, for contemporary business environments change quickly. Because this is true, scorecards need to be reviewed and changed accordingly. Further, leaders should not seek to fix all problems at the same time. Having too many directions makes it challenging for leaders to get relevant information; it also creates confusion and uncertainty. Kahneman (2012) notes that “a well-run organization will reward planners for precise execution and penalize them for failing to anticipate difficulties, and for failing to allow for difficulties that they could not have anticipated – the unknown unknown”.

Thus, introducing a scorecard 1) catalyses constructive dialogue among key stakeholders 2) improves the experience of leaders 3) encourages stakeholders to understand management reporting more deeply and 4) translates strategic imperatives into targeted action steps. Overall, the scorecard is an effective lens for management reporting because it helps leaders know where to look, what to ask, and how to interpret results.

References

Christensen et al. Competing Against Luck (USA: Harper Business, 2016).

Busco, C. & Quattrone, P. (2015) ‘Exploring how the Balanced Scorecard engages and unfolds: Articulating the visual power of accounting inscriptions’, Contemporary Accounting Research, 32(3): pp.1236–1262.

Kahneman D. Thinking, Fast and Slow (Great Britain: Penguin Books, 2012).

Kaplan R., Norton D. (1992) The Balanced Scorecard – Measures That Drive Performance, Harvard Business Review

Quattrone, P., Busco, C., Scapens, R. & Giovannoni, E. (2016) ‘Dealing with the unknown: Leading in uncertain times by rethinking the design of management accounting and reporting systems’, CIMA Academic Research Paper,12(14).